From the perspective of PMI, considering the situation related to the steel industry and downstream manufacturing, the overall demand for manufacturing rebounded in March, while the overall steel production weakened. The overall industrial steel market may be relatively strong, but it is necessary to be vigilant against the change in enterprises' tendency towards molten iron brought about by the weakening of the construction steel market.

As the most important leading indicator, the PMI index is of great significance to the steel industry. This article attempts to analyze the possible situation of the steel market in March by analyzing the PMI data of the steel industry and the manufacturing PMI.

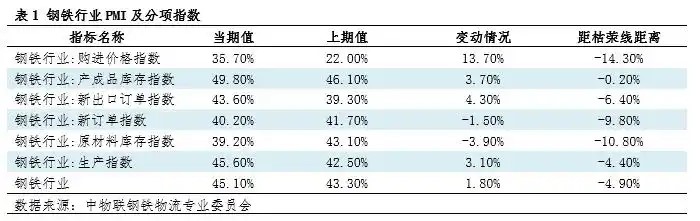

Analysis of the Steel PMI situation: The steel market continues to shrink

According to the PMI of the steel industry surveyed and released by the Steel Logistics Professional Committee of the China Federation of Logistics and Purchasing, it was 45.10% in February 2025, an increase of 1.80 percentage points compared with the previous period, but still below the 50% boom-bust line. From the perspective of sub-indexes, the purchase price index increased by 13.7 percentage points to 35.70%. Although the increase was relatively large, the support from the raw material side was even more insufficient. The production index rose from 42.50% to 45.60%, and the degree of production contraction weakened somewhat. From the demand side, the inventory of finished products was 49.80%, an increase of 3.70 percentage points compared with the previous period. The decline in inventory narrowed significantly, which might be affected by the Spring Festival factor. New export orders accounted for 43.60%, an increase of 4.30 percentage points compared with the previous month, indicating a weakened degree of market contraction. The new order index was 40.20%, a decrease of 1.50 percentage points compared with the previous period.

Overall, the main sub-indices remain below the 50% boom-bust line, and the overall steel market is weak in both supply and demand, with the shrinking state continuing. From a comparative perspective, the degree of contraction in order-related indices is still higher than that in production. Considering the expected increase in production brought about by the traditional peak demand season of March and April, the overall supply and demand pressure in the steel market may continue to increase.

Analysis of the Manufacturing PMI situation: The industrial steel market has shown an improvement in momentum

Data released by the National Bureau of Statistics' Service Industry Survey Center and the China Federation of Logistics and Purchasing shows that in February 2025, the Purchasing Managers' Index (PMI) for the manufacturing sector was 50.20%, an increase of 1.10 percentage points from the previous month, indicating that the overall manufacturing industry has shifted from contraction to expansion.

From the perspective of sub-indexes, the important production index was 52.50% this period, an increase of 2.70 percentage points compared with the previous period, above the 50% boom-bust line. The new order index was 51.10%, an increase of 1.90 percentage points compared with the previous period. In addition, the purchasing volume index reached 52.10%, an increase of 2.90 percentage points compared with the previous period. Considering that the manufacturing industry gradually returns to normal production and sales after the Spring Festival, the overall demand for industrial steel has improved, providing certain support to the demand side of steel, especially for large manufacturing enterprises, the degree of recovery is significantly higher. However, the finished goods inventory index was 48.30%, an increase of 1.80 percentage points compared with the previous period. The process of inventory reduction has slowed down. Coupled with the fact that the orders on hand and new export orders have remained below the 50% boom-bust line, the sustainability of market demand is still insufficient.

The judgment on the steel price in the later period

In light of the situation in the steel industry and downstream manufacturing, for the industrial steel market in March, the demand from the manufacturing sector has improved, and the purchase volume of steel and other products has increased. From the supply perspective, the overall production of steel mills has weakened. From the perspective of industrial steel usage alone, the supply of the steel market has decreased while demand has increased, and the pressure on market operation has significantly weakened. However, from the perspective of the overall operation of the steel industry, the insufficiency on the demand side may be more due to the delay in the resumption of work and production of construction enterprises. Considering the insufficient inertia of the construction market and the relatively smooth production transition channels among steel varieties at present, it is expected that the industrial steel market as a whole will improve in March, but the extent of improvement will be limited.

Hot News

Hot News  Contact Us

Contact Us phone:+8615314169444

mobile:+8615314169444

email:[email protected]

address:Room 305, Building B, Huachuang Ceremony Center, Jinan High-tech Zone, Jinan City, Shandong Province,China