Overview: In January, the prices of construction steel generally showed a volatile and weak trend, and the market operation was relatively cautious. As the Spring Festival holiday approaches, demand has gradually weakened. The supply and circulation sides are generally cautious. Construction steel production remains at a low level, and inventories have gradually accumulated along with the seasonal decline in demand. As of January 27th, the Myspic absolute Price Index for rebar closed at 3,478.03, a decrease of 18.51 compared with the previous period. From the overall market performance, the market transactions in January were lukewarm. The downstream market did not experience the pre-holiday inventory replenishment as in previous years. Therefore, although the overall output and inventory were lower than in previous years, the prices remained at a low level for a long time. After the Spring Festival, how will the construction steel market start and how will the market situation evolve? The author attempts to analyze it from the following aspects.

In January, domestic construction steel prices generally weakened slightly, with a significant divergence between the northern and southern markets. As of January 27th, the national average price of rebar in major cities was 3,474 yuan per ton, a month-on-month decrease of 21 yuan per ton. Among the major cities, Shanghai and Guangzhou saw their prices drop by 20 yuan per ton and 30 yuan per ton respectively, while Beijing rose by 30 yuan per ton. The market continued to show a pattern of strong north and weak south.

As of January 27th, the Mysteel long Products Index closed at 144.14, down 0.5% month-on-month and 14.23% year-on-year. The Mysteel rebar price index closed at 137.6, down 0.65% month-on-month and 14.43% year-on-year. The Mysteel wire price index closed at 151.26, down 0.66% month-on-month and 13.75% year-on-year.

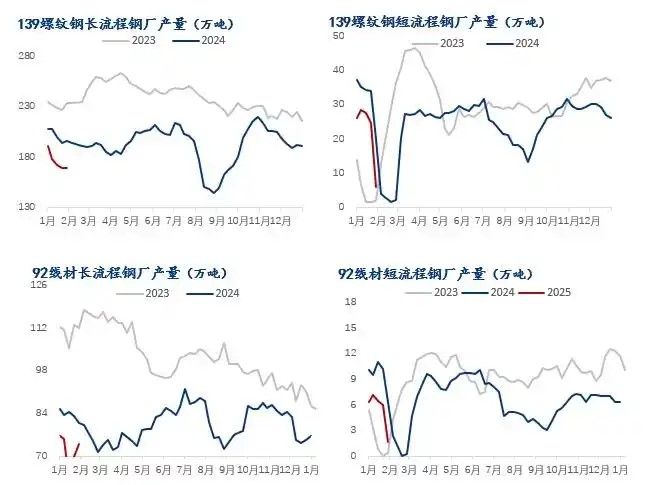

In January, the operating rate of steel mills producing construction steel across the country continued to decline. Take rebar as an example. The national operating rates have shown some differentiation. Among the seven major regions, only the operating rates in North China remained stable, while those in other regions slightly declined. Specifically, the operating rates in Northeast China, Northwest China, East China, Central China and South China decreased by 12.5%, 11.11%, 10.56%, 7.41% and 9.52% respectively compared with the previous period.

As of January 24th, the operating rate of rebar was 32.13%, a month-on-month decrease of 8.2% and a year-on-year decrease of 6.56%. The operating rate of wire rods was 41.86%, a month-on-month decrease of 5.23% and a year-on-year decline of 5.81%. By process, the operating rate of rebar in long-process enterprises decreased by 2.75% compared with the previous period, and the operating rate of long-process wire rods decreased by 0.67% compared with the previous period. The operating rate of short-process rebar decreased by 22.35% compared with the previous period, and the operating rate of short-process wire rod decreased by 38.1% compared with the previous period.

The resumption of production by steel enterprises may lead to a rational increase in output, which is likely to rise moderately

The output of construction steel continued to decline in January, mainly due to seasonal maintenance. As the resumption cycle after the Spring Festival approaches, output is expected to gradually recover in February. In the short term, the resumption process of steel mills is more constrained by the recent profit situation. If short-term profits can be maintained at the current level, the pace of steel mills' resumption of production in February is likely to accelerate. Of course, we have also noticed that since last year, steel mills have maintained a rational nature in the production of construction steel. The recovery in production in February should be moderate. Steel enterprises may arrange production in combination with inventory conditions while focusing on profits. Therefore, it is initially judged that the supply of construction steel in February will be in a state of moderate recovery.

Steel mills and social inventories may peak earlier

In January, the construction steel market entered a seasonal inventory accumulation cycle. Judging from the inventory accumulation in January, the inventory is significantly lower than in previous years. Therefore, the inventory pressure this year is not particularly high. Given that the accumulation period of inventory in previous years was around 2 to 3 weeks before and after the Spring Festival, the market gradually resumed work and production in early February this year. Therefore, it may enter a period of high inventory consolidation in the middle and late February, followed by a downward cycle. In 2025, we also need to reevaluate the relationship between inventory and output. With supply weakening in 2025, the market is likely to remain operating at a state of low output and low inventory.

Overall, the domestic construction steel market in February will operate in an environment where supply and demand gradually resume production and work. The resumption of production is certain, but the recovery of the terminal market still needs to be verified. Considering that the overall inventory level is relatively low compared to previous years, the intensity of market competition this year may not be very high. Given that the recovery of terminal demand in the first half of the month remains unclear, steel prices are more likely to fluctuate back and forth with macro and financial news. In the second half of the month, prices may gradually return to the fundamentals. Overall, it is highly likely that the prices of construction steel in February will show a volatile trend of rising first and then falling.

Hot News

Hot News  Contact Us

Contact Us phone:+8615314169444

mobile:+8615314169444

email:[email protected]

address:Room 305, Building B, Huachuang Ceremony Center, Jinan High-tech Zone, Jinan City, Shandong Province,China