In January 2025, due to the influence of multiple factors such as the approaching Spring Festival holiday and the gradual weakening of demand, the domestic steel market showed a volatile and declining trend. However, the average daily output of domestic steel in the first month of the year showed a high start. According to the statistics of the China Iron and Steel Association, in January 2025, the national daily output of pig iron was 2.267 million tons, an increase of 5.3% compared with the previous month. The daily output of crude steel was 2.642 million tons, rising by 7.9% compared with the previous period. The daily output of steel was 3.842 million tons, remaining unchanged compared with the previous period. Among them, the capacity release intensity of large and medium-sized steel production enterprises has significantly increased, and the production capacity of pig iron, crude steel and steel products has shown a month-on-month upward trend. According to the statistics of the China Iron and Steel Association, in January 2025, the daily output of pig iron by key large and medium-sized steel enterprises was 1.877 million tons, up 4.5% month-on-month, turning from a decline to an increase month-on-month, and up 2.8% year-on-year. The daily output of crude steel was 2.082 million tons, rising by 6.4% month-on-month. The month-on-month output turned from a decline to an increase, and it rose by 1.9% year-on-year. The daily output of steel was 1.965 million tons, rising by 0.4% month-on-month. The month-on-month output turned from a decline to an increase, and the year-on-year output remained unchanged.

From the perspective of the monthly steel output, the capacity release of domestic steel producers also showed a slight year-on-year decline. According to the statistics and estimates of the China Iron and Steel Association, in January 2025, the national pig iron output was 70.29 million tons, a year-on-year decrease of 3.3%. Crude steel output was 81.9 million tons, a year-on-year decrease of 5.6%. Steel output was 119.09 million tons, up 7.9% year-on-year. Among them, large and medium-sized steel enterprises produced 58.21 million tons of pig iron, 64.57 million tons of crude steel, and 60.96 million tons of steel products.

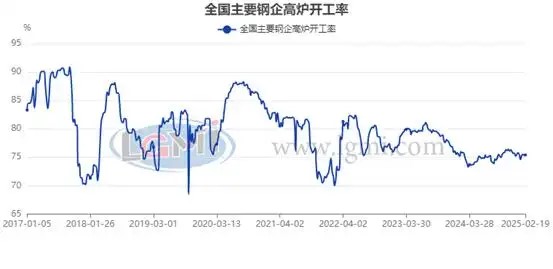

Since the beginning of February, due to the continuous swinging of the external tariff stick, the economy's deep exploration of consumption potential, the continuous increase in steel plant supply, the gradual recovery of market transactions, and the maintenance of cost support resilience and other factors, the domestic steel market has shown a distinct rangeability trend. Judging from the current changes in blast furnace operating rates, the production release intensity of steel enterprises shows a slight fluctuation trend. According to the research data from Lang Steel Network, the average operating rate of blast furnaces in 100 small and medium-sized steel enterprises across the country in the first three weeks of February 2025 was 75.4%, an increase of 0.1 percentage point compared with January. The average daily output of molten iron from 201 production enterprises across the country was 2.249 million tons, a decrease of 11,000 tons compared with the average for the entire month of January.

Judging from the ten-day production data of key large and medium-sized steel enterprises, the capacity release intensity of large and medium-sized steel production enterprises has continued to increase. According to the statistics of the China Iron and Steel Association, in the first half of February 2025, the average daily output of pig iron by key steel enterprises was 1.935 million tons, up 3.7% month-on-month and 3.0% year-on-year. The average daily output of crude steel by key steel enterprises was 2.142 million tons, rising by 3.6% month-on-month and 2.7% year-on-year. The average daily output of steel from key steel enterprises was 1.996 million tons, up 3.1% month-on-month and 2.4% year-on-year.

At present, the adverse effects brought about by changes in the external environment have deepened, while domestic demand is insufficient and there are still many risks and hidden dangers. In 2025, a variety of monetary policy tools should be comprehensively utilized. According to the domestic and international economic and financial situation and the operation of the financial market, the intensity and pace of policies should be adjusted and optimized at an appropriate time to maintain ample liquidity and ensure that the growth of social financing scale and money supply is in line with the expected targets of economic growth and the overall price level. Attention should be paid to balancing the relationships between the short term and the long term, maintaining growth and preventing risks, as well as internal and external equilibria. Based on the development of the real economy and the demands of the people for financial services, we should explore and expand the macroprudential and financial stability functions of the central bank, improve the macroprudential policy system, innovate macroprudential policy tools, promote the sustained recovery and improvement of the economy, and maintain the stable operation of the financial market. Improve real estate financial management, help the real estate market stop falling and stabilize, and support the establishment of a new model for real estate development; Enhance the forward-looking nature, pertinence and effectiveness of macro-control, strengthen the coordination and cooperation of macro policies, support the expansion of domestic demand, stabilize expectations and stimulate vitality, and promote stable economic growth.

At present, the domestic steel market is gradually transitioning from the traditional off-season to the peak season. It is expected that under the main trading logic of the frequent waving of the "tariff stick" externally and the strengthened policy expectations of the "Two Sessions" internally, coupled with the terminal demand gradually starting from the traditional "golden March" peak season, this will drive steel production enterprises to rapidly release steel production capacity. It will also become the biggest source of risk for the traditional "golden March and Silver April" steel market peak season.

Hot News

Hot News  Contact Us

Contact Us phone:+8615314169444

mobile:+8615314169444

email:[email protected]

address:Room 305, Building B, Huachuang Ceremony Center, Jinan High-tech Zone, Jinan City, Shandong Province,China