Since 2025, China's steel industry has been facing escalating external disruptions, insufficient domestic effective demand and a month-on-month increase in supply. As a result, steel prices have been fluctuating and weakening within a range, and the overall operating efficiency of the industry has been poor. Data from the National Bureau of Statistics shows that in January-February 2025, the ferrous metal smelting and rolling processing industry achieved operating income of 1,144.42 billion yuan, a year-on-year decrease of 8.5%. The operating cost was 1,102.99 billion yuan, a year-on-year decrease of 9.9%. The loss was 1.55 billion yuan.

In March, under the circumstances of continuous external tariff interference, the expected implementation of policies at the Two Sessions, the gradual recovery of downstream demand, and the continuous decline of social steel inventories, domestic steel market prices showed a volatile downward trend. However, with a slight reduction in costs and concessions, the profits of the steel industry are expected to improve compared with January-February. Looking ahead to April, the steel industry will still be in its peak season. Downstream demand will gradually be released, and external tariff disturbances will intensify. How will the business conditions of steel enterprises evolve? The Langer Steel Research Center believes that the operation of the steel industry still faces the risk of weakening in April 2025.

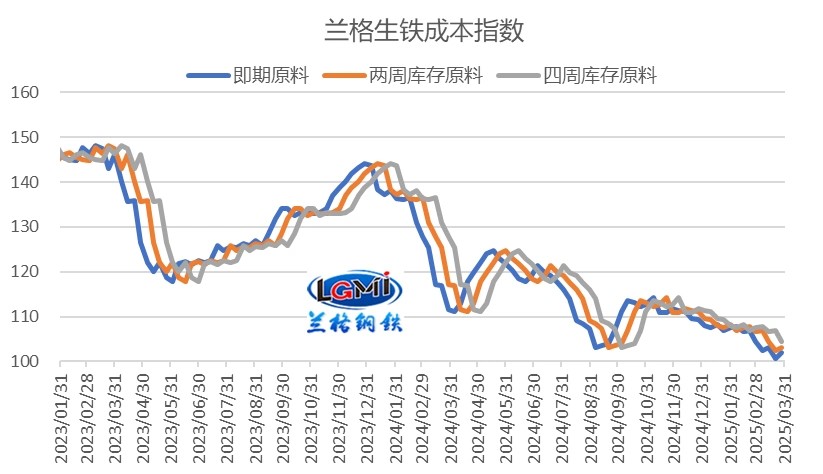

In March 2025, as the average prices of major raw materials such as iron ore, coke and scrap steel declined, the monthly average cost level continued to fall. The monthly average costs of spot costs, two-week and four-week inventory raw materials all decreased. However, the longer the inventory cycle, the smaller the decline in costs. Monitoring data from the Langer Steel Research Center shows that the cost index of pig iron calculated from spot raw materials in March was 102.0, a decrease of 4.1% compared with the same period of the previous month. The cost index of pig iron calculated from the inventory of raw materials in the past two weeks was 104.2, a decrease of 2.9% compared with the same period of the previous month. The cost index of pig iron calculated from the four-week inventory of raw materials was 106.4, a decrease of 1.0% compared with the same period of the previous month.

From a cyclical perspective, as costs gradually decline in March 2025, the profits of varieties with shorter raw material inventory cycles have improved. In terms of the average value, the monthly average value of Langer Steel's comprehensive steel price index was 3,632 yuan (per ton, the same below), a decrease of 1.2% compared with the previous month. Among them, the average monthly price of rebar was 3,393 yuan, a decrease of 2.1% compared with the previous month. The average monthly price of hot-rolled coil was 3,470 yuan, down 1.1% from the previous month. In terms of cost comparison, the estimated costs of spot and two-week inventory raw materials in March decreased relatively significantly, thus improving the profit situation of steel enterprises. However, the cost reduction in the 4-week inventory of raw materials was relatively small, and the profits of enterprises with a long raw material inventory cycle were relatively weak.

From the perspective of grade three rebar, the average monthly gross profit margins of the spot raw materials, two-week inventory raw materials, and four-week inventory raw materials of grade three rebar in March were 97 yuan, 50 yuan, and 1 yuan respectively, increasing by 17 yuan, decreasing by 12 yuan, and decreasing by 64 yuan compared to the previous month. Due to the fluctuating and downward trend of raw material prices, the length of the raw material inventory cycle has a significant impact on profits. The profit margins of enterprises with raw material inventory cycles of two weeks and four weeks have narrowed.

From the perspective of hot-rolled coil, the estimated gross profit of hot-rolled coil in March has rebounded. The estimated profit of spot raw materials is 19 yuan, turning from loss to profit. The average monthly loss calculated based on the inventory of raw materials over the past two weeks was 29 yuan, a reduction of 36 yuan compared to the previous month. The average monthly loss from the inventory of raw materials over the past four weeks was 77 yuan, an increase of 9 yuan compared to the previous month.

Based on the gross profit performance of each variety calculated from the four-week inventory of raw materials, the gross profit of the varieties calculated from the four-week inventory of raw materials in March showed a trend of first decreasing and then increasing. The average monthly profit of all varieties except medium and heavy plates declined. Monitoring data from the Langer Steel Research Center shows that among the seven monitored varieties, the average monthly profit of building materials has weakened the most, reaching 58 to 64 yuan. The gross profit margin of billets and cold-rolled coil decreased the least, at 8 to 10 yuan. The gross profit margins of other varieties declined moderately, ranging from 22 to 34 yuan.

Overall, under the combined influence of a slight decline in the prices of special materials and the downward shift in production costs, the gross profit per ton of steel calculated for spot, two-week and four-week inventory raw materials of special materials in March showed some differentiation. The profits of medium and short-cycle inventory raw materials improved, while the profits of long-cycle inventory raw materials mostly weakened. It is expected that the profit data of steel enterprises to be released in March may show a small amount of profit.

April is approaching, and the situation facing the steel industry is more complex and changeable.

From the perspective of the international environment, the US tariffs and global trade protection have intensified. On April 2nd, US President Trump announced at the White House the imposition of so-called "reciprocal tariffs" on trading partners. The United States imposes a 34% reciprocal tariff on China and levies reciprocal tariffs ranging from 10% to 46% on other countries. The tariff will come into effect at 0:01 a.m. Eastern Time on April 9. Starting from April 9th, the United States imposed an additional 50% tariff on Chinese goods and imposed tariffs of up to 104% on some Chinese goods. The United States' imposition of tariffs on the world will have a significant impact on the global industrial and supply chains. The global manufacturing PMI is showing a downward trend, and the recovery of the global economy is weakening. This will impose certain constraints on the global capital market and the commodity market, and cause considerable disturbances to China's international trade and market situation.

From the perspective of the domestic environment, under the circumstances of intensified external uncertainties, China will dynamically adjust policies based on the degree of external influence, strengthen extraordinary counter-cyclical regulation, and enhance the forward-looking, targeted and effective nature of macro-control. On April 4th, China issued a number of countermeasures against the United States, imposing a 34% tariff on all imported goods from the United States, suing the US for related practices under the World Trade Organization's dispute settlement mechanism, placing several US entities or enterprises on the export control list or unreliable entity list, and implementing export controls on related items of medium and heavy rare earths, etc. In the future, China will introduce monetary policy tools such as reserve requirement ratio cuts and interest rate cuts at any time as the situation demands. Fiscal policy has clearly stated that the intensity of expenditure should be increased and the pace of expenditure accelerated. There is still room for further expansion of fiscal deficits, special bonds, and special Treasury bonds, depending on the situation. We will boost domestic consumption with extraordinary efforts, accelerate the implementation of established policies, and introduce a batch of reserve policies in due course. We will resolutely stabilize the capital market and market confidence with concrete policy measures. Relevant contingency plans and policies will be successively introduced.

From the supply side of the steel industry, in January-February, the capacity release of steel enterprises remained relatively stable year-on-year. It is expected that domestic steel output in March will continue to rise slightly compared with January-February. According to the estimation of the Lang Steel Research Center, the national crude steel daily output in March is expected to rise to around 2.85 million tons.

From the demand side, with the overall improvement of climatic conditions, the demand for steel will be further released. It is expected that the demand for construction steel will continue to recover in April, and the prosperity of the manufacturing industry will continue to rise. The overall demand for steel from downstream is still expected to be released steadily.

From the cost perspective, the average price of raw materials dropped in March, and the average monthly production cost of steel decreased, weakening the support of costs for steel prices.

Overall, factors such as the implementation of both existing and new policies for stabilizing domestic economic growth, the continuous release of demand during peak seasons, and the sustained decline in social steel inventories have provided support to the market. However, the intensification of external tariff disturbances and the weakening of global economic recovery have exerted strong external suppression on the steel market. The Langer Steel Big Data AI-assisted decision-making System predicts that It is expected that the domestic steel market may show a volatile and pressure-bearing operation trend in April 2025.

From the perspective of steel enterprises' profits, under the volatile and pressure-bearing operation of the steel market in April 2025, the temporary downward pressure on prices still exists. The Lang Steel Research Center predicts that the operating profits of steel enterprises in April 2025 will remain weak and there may be a risk of a temporary deterioration.

Hot News

Hot News  Contact Us

Contact Us phone:+8615314169444

mobile:+8615314169444

email:[email protected]

address:Room 305, Building B, Huachuang Ceremony Center, Jinan High-tech Zone, Jinan City, Shandong Province,China