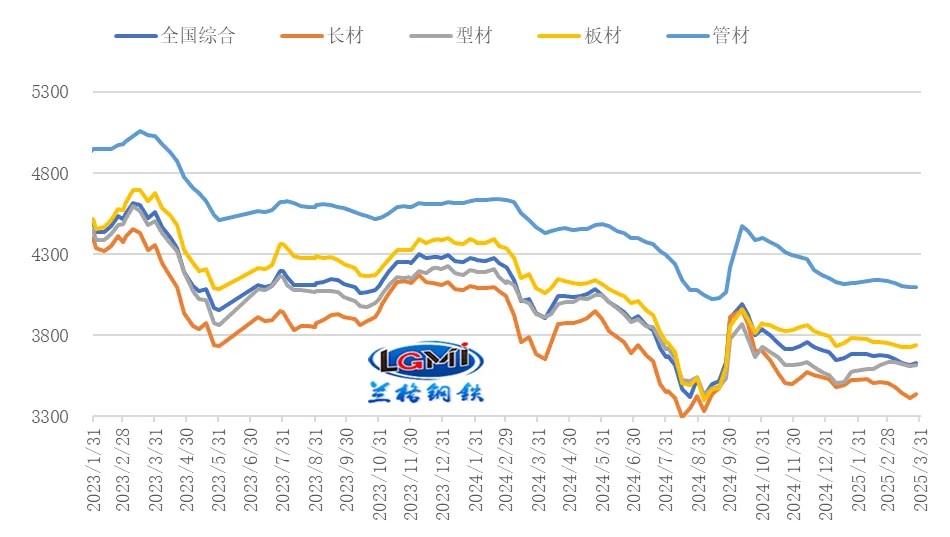

In March 2025, under the circumstances of continuous external tariff interference, the implementation of the expected policies of the Two Sessions, the gradual recovery of downstream demand, the continuous decline of social steel inventory, and a slight downward shift in the cost side, the domestic steel market price showed a volatile downward trend, with the average price dropping compared to the previous month. According to the monitoring data of Lang Steel Network, as of the end of March, the average comprehensive price of steel across the country of Lang Steel was 3,633 yuan per ton, a decrease of 43 yuan per ton compared with the previous month, with a month-on-month decline of 1.2% and a year-on-year decline of 8.3%. In terms of the monthly average, in March, the national average comprehensive price of steel of Lang Steel was 3,633 yuan per ton, a decrease of 43 yuan per ton compared with the previous month, representing a decline of 1.2%.

Looking ahead to April, from an international perspective, the global manufacturing PMI continues to show a stable recovery, the global economy maintains a steady recovery trend, and its internal resilience has become somewhat evident. Inflation in various countries has dropped again. The expectation of the Federal Reserve cutting interest rates still exists, coupled with the slowdown in the pace of balance sheet reduction, which will provide certain support to the commodity market. Domestically, the policy goals of the Two Sessions are in line with expectations and will be gradually implemented in the future. In the next stage, the country will implement more proactive and effective macro policies, comprehensively expand domestic demand, and promote the sustained recovery and improvement of the economy. In April, as the downstream demand for steel continues to recover, the social inventory of steel will continue to be reduced, and the market price of steel is expected to show a rebound trend. However, the cost support will weaken, and the external tariff pressure will still impose significant constraints on the market. It is necessary to be vigilant about the momentum of its impact. The Langer Steel Big Data AI-Assisted Decision-making System predicts that the domestic steel market is expected to show a volatile but slightly strong operating trend in April 2025.

The main driving factors for the relatively strong fluctuations in domestic steel market prices in April are as follows:

First, the global economy maintains a steady recovery, providing certain support for the commodity market

At present, the global manufacturing PMI shows a continued and stable recovery trend. According to data from jpmorgan Chase, in February 2025, the jpmorgan Global Manufacturing PMI Index was 50.6%, rising by 0.5 percentage points compared with the previous month. Among them, both the output index and the new order index rebounded. The output index rose by 0.9 percentage points compared with the previous month to 51.5%. The new order index was 51.3%, rising by 0.5 percentage points compared with last month. During the same period, the China Federation of Logistics and Purchasing released data showing that the global manufacturing PMI in February was 50.0%, remaining the same as the previous month. At present, the global economy continues to maintain a steady recovery trend, and its inherent resilience has emerged to some extent.

From the perspective of CPI in various countries, the inflation data in February 2025 declined somewhat. The CPI in the United States in February was 2.8%, down 0.2 percentage points from the previous month. The core CPI in the United States was 3.1%, down 0.2 percentage points from the previous month. The CPI in the eurozone rose by 2.4% year-on-year in February, down 0.1 percentage point from the previous month.

The Federal Reserve announced on March 19 local time that it would keep the benchmark interest rate unchanged at 4.25%-4.5% and indicated that it might cut interest rates within the year. Meanwhile, the Federal Reserve adjusted its economic growth expectations and slowed down the pace of reducing its balance sheet (quantitative tightening, QT). The rising expectations of the Federal Reserve cutting interest rates have weakened the appeal of the US dollar. The slower pace of balance sheet reduction helps ease the liquidity pressure in the market and indirectly supports the commodity market.

Second, domestic policies to stabilize growth have been continuously implemented and put into practice, supporting market confidence

In 2025, China's fiscal policy will be more proactive. The fiscal deficit ratio is planned to be set at around 4%, an increase of 1 percentage point over the previous year. The deficit scale will be 5.66 trillion yuan, an increase of 1.6 trillion yuan over the previous year. The scale of general public budget expenditure was 29.7 trillion yuan, an increase of 1.2 trillion yuan over the previous year. It is planned to issue 1.3 trillion yuan of ultra-long-term special Treasury bonds, an increase of 300 billion yuan compared with the previous year. It is planned to issue 500 billion yuan of special Treasury bonds to support large state-owned commercial banks in replenishing their capital. It is planned to allocate 4.4 trillion yuan of local government special bonds, an increase of 500 billion yuan compared with the previous year. The bonds will mainly be used for investment and construction, land acquisition and storage, purchase of existing commercial housing, and digestion of local government debts owed to enterprises. This year, the total scale of newly added government debt amounts to 11.86 trillion yuan, an increase of 2.9 trillion yuan compared with the previous year. The intensity of fiscal expenditure has significantly increased.

In March, the General Office of the Central Committee of the Communist Party of China and The General Office of the State Council issued the "Special Action Plan for Boosting Consumption". On March 17, the Information Office of The State Council held a press conference on boosting consumption. Li Chunlin, vice minister of the National Development and Reform Commission, introduced that in 2025, 300 billion yuan of ultra-long-term special Treasury bonds will be allocated to support the expansion of the trade-in program for consumer goods. This amount has doubled compared to last year, and the first batch of 81 billion yuan has been distributed to local authorities since early January.

At present, the external environment that our country is facing is more complex and severe, with many unstable and uncertain factors. Domestic demand is relatively weak, and some enterprises still encounter many difficulties in production and operation. In the next stage, we will earnestly implement the spirit of the Central Economic Work Conference and the Two Sessions, adopt more proactive and effective macro policies, comprehensively expand domestic demand, strengthen innovation-driven development, deepen reform and opening up, promote sustained economic recovery and improvement, and effectively ensure and improve people's livelihood.

Thirdly, domestic steel demand is still in its peak season

In March 2025, the transaction volume of building materials recovered significantly. According to the statistics of Langang Steel Network, the average daily transaction volume of construction steel in 20 key cities in March was 139,500 tons (see Figure 2), an increase of 45,800 tons compared with the previous month, but a year-on-year decrease of 5.2%. Fiscal policy in 2025 should be more proactive, sustained and effective. In terms of special bonds, the issuance of special bonds has been accelerated in 2025. Data shows that as of March 25th, the scale of new special bonds issued by various regions this year reached 801.615 billion yuan, an increase of 75.56% compared with the same period in 2024. The scale of refinancing special bonds used to replace existing implicit debts has reached 1,288.442 billion yuan, and the issuance progress compared with the 2 trillion yuan quota this year has reached 64.42%. In April, as weather conditions further improve, the construction of building projects will accelerate, and the demand for construction steel will continue to recover and be released.

In March, the monthly shipment volume of sheet products continued to recover. According to the March shipment data statistics of Langang Steel Network, the average monthly shipment volume of hot-rolled coil in 16 key cities across the country was 44,700 tons (see Figure 15), an increase of 5,100 tons compared with the previous month, with a month-on-month growth of 12.9% and a year-on-year growth of 29.2%. The average daily shipment volume of medium and heavy plates from 105 key circulation enterprises in 15 key cities across the country was 54,200 tons, an increase of 7,800 tons compared with the previous month, rising by 16.8% month-on-month and 19.9% year-on-year. The manufacturing industry's prosperity picked up significantly in March, and it is expected that the demand for steel in the manufacturing sector will maintain a certain degree of resilience in April 2025.

Hot News

Hot News  Contact Us

Contact Us phone:+8615314169444

mobile:+8615314169444

email:[email protected]

address:Room 305, Building B, Huachuang Ceremony Center, Jinan High-tech Zone, Jinan City, Shandong Province,China