Overview: Looking back at the performance of the seamless pipe market since the Spring Festival, the overall price of seamless pipes has shown a weak downward trend. The supply from pipe factories has continued to rise, while the recovery of downstream demand has been somewhat differentiated. The progress of infrastructure projects has been relatively slow, and the demand from manufacturing, oil and gas, etc. has risen simultaneously. Seamless pipe merchants are relatively cautious in their mindset, keeping their overall inventory at a reasonable level. Most merchants mainly focus on risk control. Entering the traditional peak season of "Silver April", how will the seamless pipe market perform? Will there be a phased trend in the seamless pipe market in April? The following is a brief analysis by the author.

I. Technical aspect: Price bottoming out and cost support

1. Price cycle and bottom signals

As of the end of March 2025, the national average price of seamless steel pipes was 4,393 yuan per ton, a month-on-month decline of 40 yuan per ton and a year-on-year decline of 441 yuan per ton. The current price is at a relatively low level in the past five years, below the historical median line. From a technical perspective, the current price range is at a relatively low level, with limited downward space for the technical aspect, which provides certain support for the price of seamless pipes. Historical data shows that in April, prices mostly fluctuated or rose.

Profit recovery drives the willingness to hold prices

Based on the current raw material prices, as of the end of the month, the national tube billet price was reported at 3,493 yuan per ton, a year-on-year decline of 286 yuan per ton. The price difference between tube billets and square billets remained at 410 yuan per ton. Currently, the valuation of tube billet prices is relatively high, providing certain support to seamless pipe factories. In 2024, the profits of pipe factories contracted significantly, with some enterprises approaching the loss line. In the first quarter of 2025, the profits of seamless pipe factories (billet type pipe factories) mostly remained inverted. Under the strong support of raw materials and low profits, the pipe factories' willingness to hold prices was relatively strong in April.

Ii. Fundamentals: Marginal improvement in supply and demand supports prices

1. Supply side: Environmental protection production restrictions curb the release of production capacity

In 2025, the production restriction policy during the non-heating season will become regular (such as in the Beijing-Tianjin-Hebei region and Tangshan, etc.), coupled with the increasingly strict environmental supervision, the release of seamless pipe production capacity in the later period will be restricted. Although the overall production capacity of the industry still shows an expanding trend, short-term output may be suppressed, and the pressure on factories and warehouses has eased somewhat, providing space for a price rebound.

2. Demand side: Seasonal peak season and structural increment

The traditional peak season effect: April is the "Silver April" construction peak season. As temperatures rise in the north, the operation rate of construction sites increases, infrastructure projects accelerate their progress, and the demand for seamless pipes is expected to grow month-on-month.

Structural demand resilience: Incremental demand still exists in areas such as oil and gas pipeline networks and power and heat engineering. In particular, energy projects in the "Belt and Road" countries have a significant driving effect on China's seamless pipe exports.

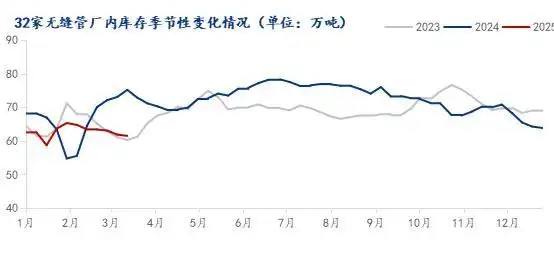

The inventory pressure has been gradually digested. By the end of the first quarter, the social inventory of seamless steel pipes was at a low level in nearly three years. The active inventory reduction strategy of traders took effect, and market risk appetite rebounded. If the pace of demand release in April is in line with expectations, the accelerated digestion of inventory will further support the price of seamless pipes. Iii. Macro Aspect: Policy benefits resonate with expectations of demand recovery

Policies to stabilize the economy have continued to take effect

By the end of the first quarter of 2025, domestic macro policies will focus on "stabilizing growth", including cutting the reserve requirement ratio and interest rates, optimizing real estate policies (such as adjusting the interest rates of existing mortgage loans and easing purchase restrictions), and accelerating infrastructure investment. These measures will directly stimulate the downstream demand for steel, especially in seamless pipe application scenarios such as pipeline renovation and water conservancy projects in the infrastructure sector. In addition, the strengthening of expectations for global economic recovery and the stabilization of international oil prices may drive up the demand for oil and gas drilling pipes and support the resilience of exports. The liquidity environment has improved, domestic fiscal funds have gradually been channeled to the real economy, and market confidence in bulk commodities has been somewhat restored. The stabilization of the macro environment helps ease the pessimism in the seamless pipe market and drive prices to bottom out and rebound.

Iv. Comprehensive Prediction:

Overall, the price of seamless steel pipes in April 2025 is likely to show a trend of "fluctuating slightly upward" :

Price range: It is expected that the national average price will be between 4,450 and 4,550 yuan per ton (taking 20# and 108*4.5mm as examples), an increase of approximately 50 to 100 yuan per ton compared to March.

The driving logic: The triple benefits of macro policy support, peak season demand release, and inventory pressure relief resonate, but overcapacity and export uncertainty restrict the increase.

Operation suggestion: Traders can replenish inventory at low prices and pay attention to the pace of inventory reduction. Terminal enterprises should be vigilant against the risk of price pullbacks after a sharp increase and mainly purchase as needed.

Hot News

Hot News  Contact Us

Contact Us phone:+8615314169444

mobile:+8615314169444

email:[email protected]

address:Room 305, Building B, Huachuang Ceremony Center, Jinan High-tech Zone, Jinan City, Shandong Province,China